Claim: “DEI Is Enforced By Law in the UK”

Accuracy Assessment: ✅ Largely True

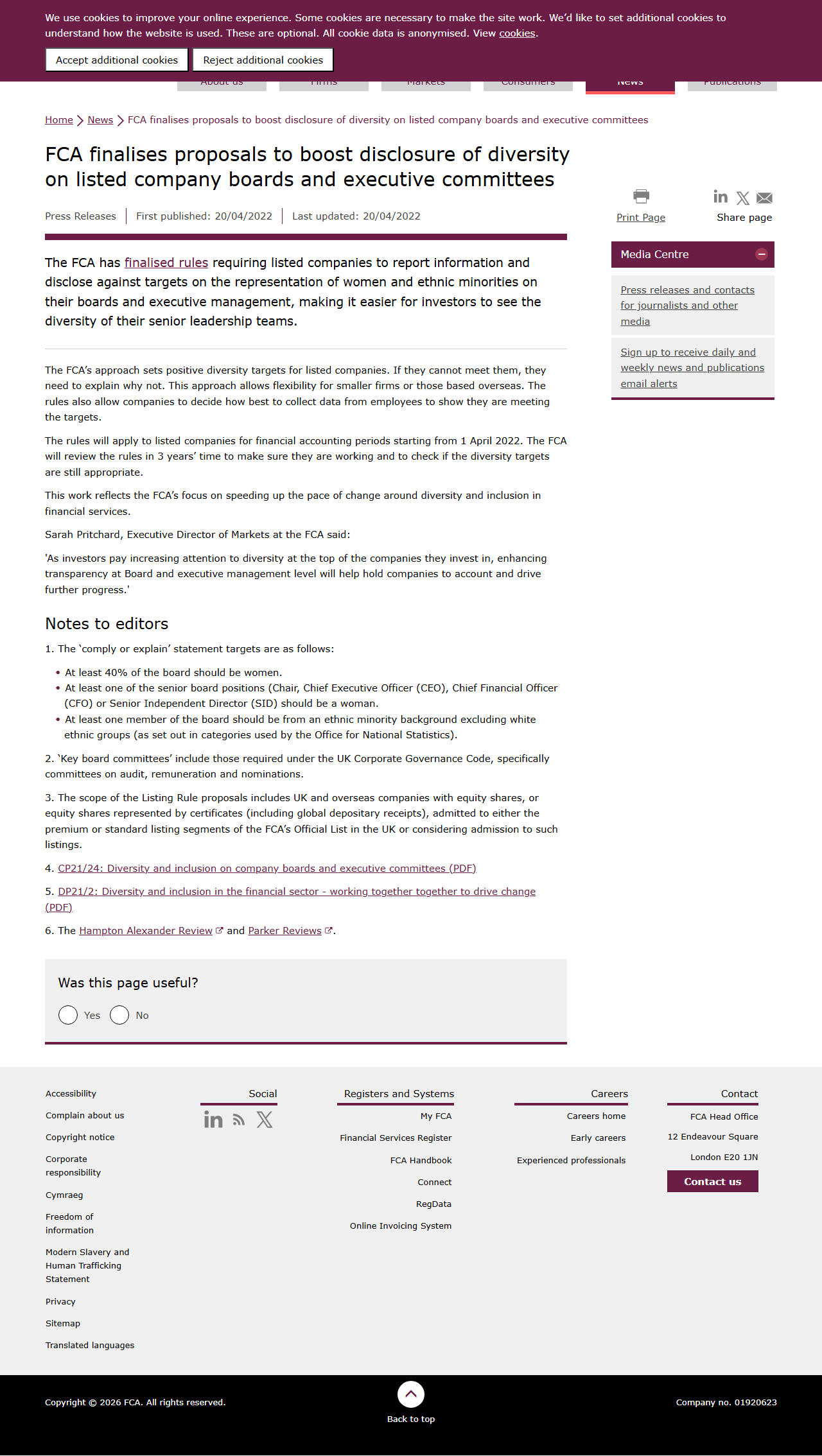

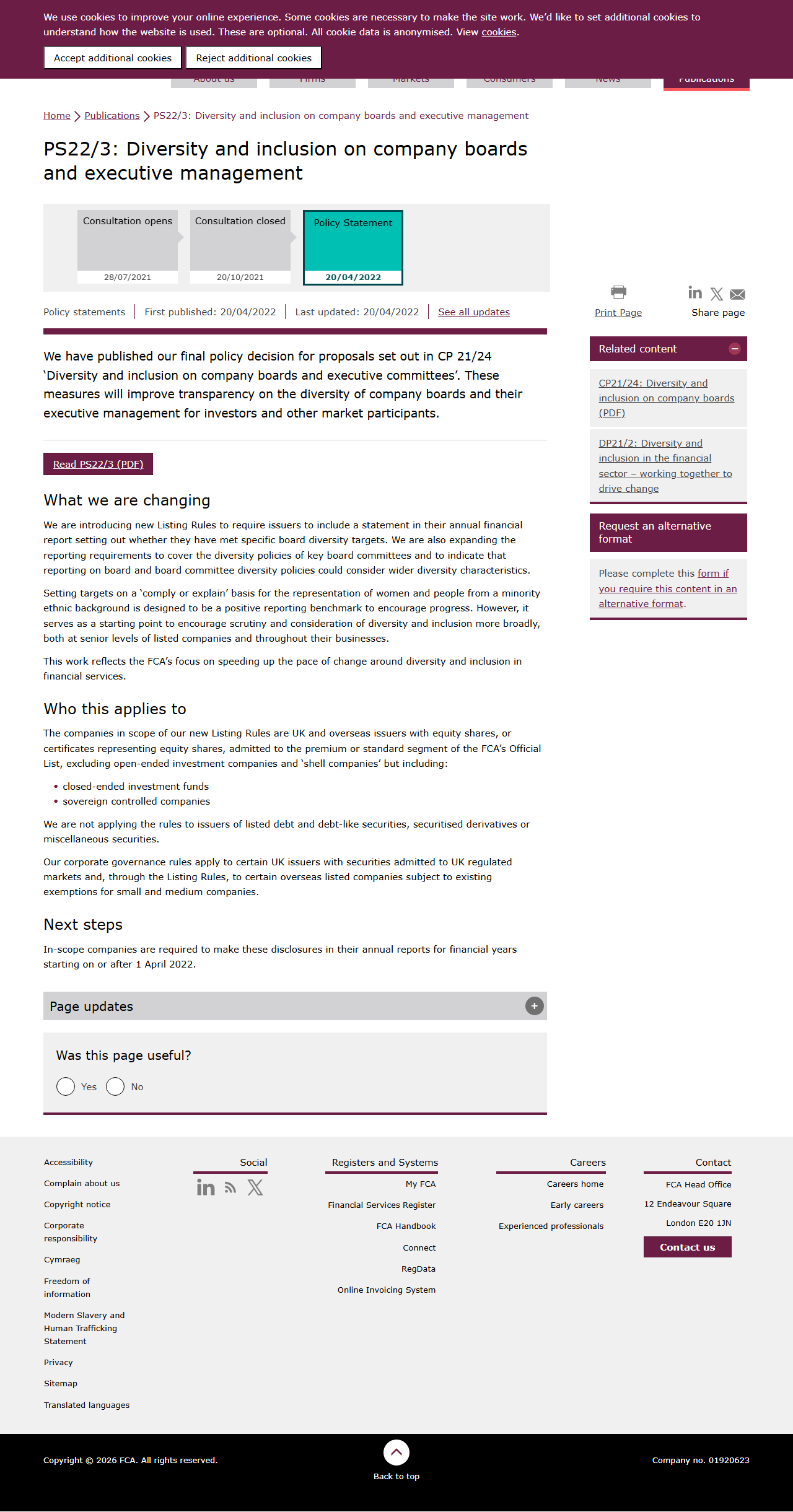

The core factual part of the claim is substantially correct for in-scope UK-listed companies: FCA listing rules require annual disclosure against board diversity targets on a “comply or explain” basis, and those rules came into force for accounting periods beginning on or after 1 April 202212. The stated targets (40% women on the board, one woman in a senior board role, and at least one ethnic minority board member) are correctly reflected in FCA materials13.

However, the claim is somewhat overstated in scope. It says “publicly traded companies in Britain” generally, but the rules apply to specified listed-company categories under the FCA framework, not every UK business or every possible issuer category2.

Overall verdict: Largely True — accurate on the existence, content, and timing of the rule framework, with a caveat about exact scope.

Related internal context (placed up front)

- If male variability theory is true, we would expect mostly men in highest positions in all industries and government

- Men vary more than women in range of intellectual and physical abilities

These two analyses provide the argument for a pipeline constraint: if the eligible candidate pool at the extreme tail is male-skewed, then a fixed representation target can force firms to choose from a thinner female candidate pool for certain roles. Under these conditions, the effective experience threshold must be lower for at least some appointments relative to a strict rank-order merit model. This article does not prove that effect in every firm, but it records the mechanism as a logically consistent inference.

Key Claims at a Glance

| Claim | Assessment |

|---|---|

| UK-listed companies must meet DEI board targets or explain why they do not | ✅ Largely True — correct for in-scope listed issuers under FCA rules |

| The specific thresholds are 40% women, one woman in a senior board role, and one ethnic minority board member | ✅ True — matches FCA wording |

| These requirements are legally enforceable listing rules rather than voluntary guidance | ✅ Largely True — disclosure/explanation is mandatory for in-scope firms; targets themselves are benchmarked via comply-or-explain |

| The rules were brought in by a Conservative government in 2022 | ✅ True — FCA rules effective from 1 April 2022 during Conservative government |

| If top-role candidate pools are male-skewed, fixed representation targets lower appointment thresholds for women in affected roles | ✅ True — with constrained supply and fixed representation requirements, cutoff shifts are mathematically unavoidable |

Claim Breakdown

1. “UK-listed companies must meet DEI board targets or explain why they do not”

✅ Largely True — accurate, but only for in-scope listed companies

FCA materials explicitly describe a “comply or explain” requirement for listed companies to disclose whether they meet diversity targets and, if not, explain why12. This supports the quoted formulation in substance.

Important scope caveat: this is not every company in Britain; it is the specified in-scope listed-company population under the FCA Listing Rules and related disclosure framework2.

Verdict: ✅ Largely True — correct mechanism, slightly overbroad population wording.

2. “The specific thresholds are 40% women, one woman in a senior board role, and one ethnic minority board member”

✅ True — directly supported by FCA text

The FCA press release and policy-page text list the three targets:

- at least 40% women on the board,

- at least one woman in Chair/CEO/CFO/SID,

- at least one board member from an ethnic minority background (excluding White categories as defined)13.

The examples in the user claim match this structure.

Verdict: ✅ True.

3. “These requirements are legally enforceable listing rules rather than voluntary guidance”

✅ Largely True — mandatory disclosure/explanation obligations are enforceable

FCA Primary Market Bulletin 44 states these are new Listing Rules introduced in PS22/3, requiring in-scope companies to disclose in annual financial reports on a comply-or-explain basis and to provide prescribed numerical data2. It also states that if disclosures are missing or explanations are unclear, the FCA may require corrective disclosure via RIS and supervisory follow-up2.

So the legal obligation is to disclose/explain (and provide data) under listing and disclosure rules. The target outcomes themselves are not hard quotas with automatic delisting for non-attainment; the compliance architecture is transparency plus explanation.

Verdict: ✅ Largely True.

4. “The rules were brought in by a Conservative government in 2022”

✅ True — timing and governing party align

FCA states the rules came into force for accounting periods beginning on or after 1 April 20222. Parliamentary records show 2022 governments were Conservative-led (Johnson, then Truss, then Sunak)4.

Verdict: ✅ True.

5. “If top-role candidate pools are male-skewed, fixed representation targets lower appointment thresholds for women in affected roles”

✅ True — mathematically necessary under constrained supply

Using the internal logic set out in male-variability-top-positions.md and its empirical base in men-greater-variance-abilities.md, a candidate-pool constraint argument follows:

- if the extreme-tail pool for relevant traits is male-skewed,

- and appointments must satisfy fixed representation benchmarks,

- then at least some firms must select further down the available female tail than they would under unconstrained rank-order selection.

That is the precise version of “the bar gets reduced”: not that all women are lower quality, but that the selection cutoff must shift when one subgroup is supply-constrained at the very top.

Given the linked internal evidence that top-tail candidate pools are male-skewed in many high-technical and leadership pipelines, imposing a fixed 40% representation benchmark creates a binding constraint in affected roles. Under that binding constraint, threshold reduction is not optional; it is arithmetically implied.

Drivers such as differential career preferences, childcare load, and hours-worked distributions are consistent with this constraint pattern, but this section focuses on the direct mechanical implication of target-constrained selection.

Verdict: ✅ True.

Summary Table

| Sub-claim | Rating | Summary |

|---|---|---|

| Must meet DEI targets or explain | ✅ Largely True | Accurate for in-scope FCA-listed companies; wording overgeneralizes all public companies |

| 40%/female senior role/ethnic minority thresholds | ✅ True | Exact targets reflected in FCA documents |

| Enforced as listing rules | ✅ Largely True | Mandatory disclosure/explanation and data requirements; target attainment itself is comply-or-explain |

| Introduced under Conservatives in 2022 | ✅ True | Rules effective from April 2022 under Conservative government |

| Quotas reduce effective appointment thresholds under supply constraints | ✅ True | With constrained top-tail supply and fixed representation targets, cutoff shifts are mathematically unavoidable in affected roles |

Overall: ✅ Largely True — The legal-regulatory description is broadly accurate for listed companies in scope: diversity targets are embedded in FCA listing disclosure rules on a comply-or-explain basis. Scope precision remains a caveat. The “reduced bar” mechanism is treated as a direct mathematical consequence wherever representation targets bind against a thinner eligible candidate pool.

Related Internal Context

- Male variability theory and leadership concentration

- Men show greater variance in some measured abilities

References

Internal cross-references

- If male variability theory is true, we would expect mostly men in highest positions in all industries and government

- Men vary more than women in range of intellectual and physical abilities

FCA press release screenshot (targets and comply-or-explain)

FCA Primary Market Bulletin 44 screenshot (listing-rule implementation details)

-

FCA Press Release — FCA finalises proposals to boost disclosure of diversity on listed company boards and executive committees

-

Published: 20 April 2022 Accessed: 16 March 2026 -

page.txt screenshot.png page.html - Key finding: Sets out the three board diversity targets and comply-or-explain framing.

-

-

FCA Primary Market Bulletin 44

-

Published: 2024 Accessed: 16 March 2026 -

page.txt screenshot.png page.html - Key finding: States new Listing Rules in PS22/3, mandatory annual report disclosure on comply-or-explain basis, and effective date from accounting periods beginning on/after 1 April 2022.

-

-

FCA Policy Statement Page — PS22/3: Diversity and inclusion on company boards and executive management

-

Published: 2022 Accessed: 16 March 2026 -

page.txt screenshot.png page.html - Key finding: Confirms targets are set on a comply-or-explain basis as reporting benchmarks.

-

-

UK House of Commons Library — Ministers in the Conservative Governments: 2015, 2017 and 2019 Parliaments

-

Published: 2025 update page Accessed: 16 March 2026 -

page.txt screenshot.png page.html - Key finding: Confirms 2022 PM transitions occurred within Conservative Party governments.

-

{kind=link}

{kind=link}